by Marc Cohen, Director of the Center on Long-Term Services and Supports

On November 30, I was invited to testify before the Subcommittee on Government Operations of the Committee on Oversight and Government Reform. The committee examined why employees participating in the federal long-term care insurance program were experiencing such large rate increases and what might be done to make program premiums more predictable and stable. Participants on the panel included representatives from the Office of Personnel Management, John Hancock Insurance Company, and the National Association of Retired Federal Employees.

Members of the Congressional committee were particularly concerned about the hardship placed on policyholders of increasing premiums and discussed the broader implications for the market as a whole. The key challenge identified was that premium increases across the market have made the product too costly for a growing number of middle-income consumers who only have personal savings and safety net programs like Medicaid to rely on should they require significant amounts of care. My own view is that the underdevelopment and growing unaffordability of private insurance and the absence of any public insurance presents a fundamental problem: people have no way to plan effectively for what is actually an insurable risk, which is why fewer than 10% have insurance for long-term services and supports (LTSS).

During the hearing I pointed out that rate increases should be viewed within the broader context of the long-term care insurance market and the challenges faced by all insurers in that market. Actuaries are still learning how the product is performing and they are therefore making adjustments to their initial pricing assumptions. I also emphasized that there is a critical need for an insurance-based solution for middle-class Americans, many of whom will face catastrophic costs and financial impoverishment in the absence of insurance solutions.

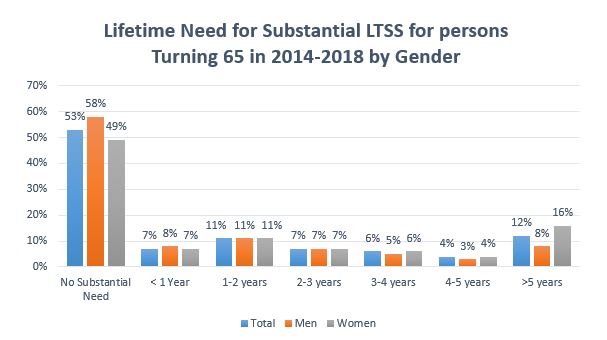

The reason that insurance makes sense for long-term services and supports (LTSS) is because there is a relatively small probability of a long period of impairment and associated costs, and individuals lack the ability to predict in advance whether they will have such an event. While roughly half the population age 65 and over will never need substantial support, roughly one in five who have at least two or more limitations in activities of daily living, will need assistance for between two and five years and just over one in ten will need care for more than five years–which could cost upwards of $250,000.

Source: Favreault, M. & Dey, J. (2015) Long-Term Services and Supports for Older Americans: Risks and Financing Research Brief, U.S. Department of Health and Human Services.

I tried to emphasize that without public support, due to a variety of demand and supply factors, the private insurance market alone is unlikely to play a meaningful role in financing the nation’s LTSS needs. After reviewing for the committee a number of the reasons why so many insurers have left the market and so few people have policies (e.g. selling costs are high, consumers lack knowledge and understanding about LTSS risks and costs, they are confused about the role of public programs, there is general mistrust of insurers, insurers face a variety of unpredictable and often uncontrollable risks that are hard to spread, premium structures are highly unstable given the need to make predictions about interest rates, and LTSS needs 20-30 years into the future), I put forward my view that an insurance-based public/private partnership stands the best chance of moving the needle on protecting middle-class Americans from significant costs that threaten their retirement. I also suggested that in addition to an educational campaign designed to reduce consumer confusion and increase awareness and knowledge and changes in the product itself, the federal or state governments may want to consider an insurance program for catastrophic LTSS risk which would provide a base that the private insurance industry could supplement or “wrap around.”

My strong belief, based on years of working with the industry and policymakers, is that this would likely encourage more insurers to get back into the market, broaden the risk pool, lower the cost of insurance products, and provide consumers with a real opportunity to plan and protect themselves against LTSS costs–the largest unfunded liability during retirement.

Marc Cohen (PhD, Brandeis) serves as director of the new Center for Long-Term Services and Supports at the McCormack Graduate School’s Gerontology Institute and research director at our partner organization, the Center for Consumer Engagement and Health System Transformation, Community Catalyst. His areas of expertise include financing long-term services and supports, private long-term care insurance, fall prevention, service utilization patterns of disabled elders, family caregiving, care management and care transitions, and managing long-term services and supports populations.

December 30, 2016 at 1:49 pm

Good points but might have also described how in the early years rating was guesswork and based on competitive issues with strict benefit criteria (skilled facilities). High interest rates contributed to less rate pressure. As the public objected benefits got less restrictive while interest rates dropped but actuarial assumptions required by regulators did not reduce. Unlike other medical lines in which benefit adjustments could help reign in rates, rate increases erected the only alternative.